Protests in Iran are threatening to disrupt the country’s upstream sector and highlighting a deeper economic crisis, according to Rystad Energy analysis

Iran has restored output and exports despite sanctions, but at a rising cost: deeper discounts to China, expensive ‘shadow’ logistics and shrinking fiscal buffers, including the running down of its National Development Fund (NDF).

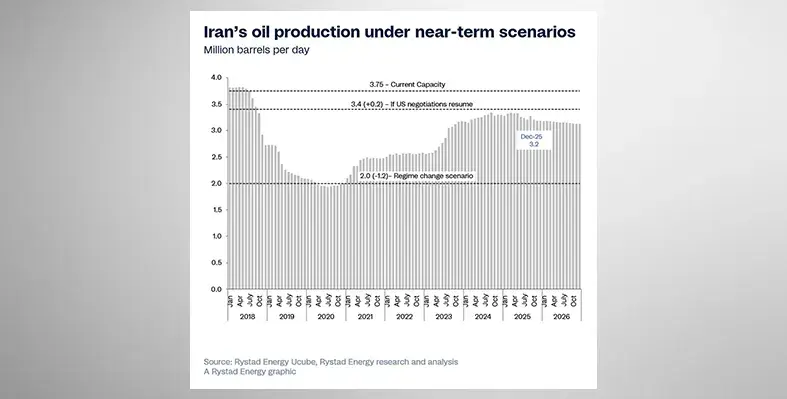

Iranian crude production is expected to remain stable at around 3.2mn bpd this year, according to Rystad, with limited short-term disruption to upstream operations, despite significant financing and redevelopment hurdles. The greater risk currently is the geopolitical risk premium as tensions rise and uncertainty persists. With the US administration of President Donald Trump exerting maximum economic pressure on Iran’s trading partners and threatening military intervention, the Middle Eastern oil giant will likely entrench itself even further.

“Iran’s familiar tactics, such as closing the Strait of Hormuz, banking on its trade with China and threatening nuclear escalation, are still on the table, yet must be weighed by their own potential for backfiring on the regime. Economically, Iran has been cornered by heavy sanctions, yet the country has managed to protect what limited revenue remains. Although the US has announced that it will impose a 25% tariff on countries that trade with Iran, China’s crude buying patterns are expected to remain stable. China has an established practice of sourcing discounted barrels from sanctioned producers, and Iran has a proven ability to sustain exports through sanctions evading trade networks. For the status quo to be truly disrupted, external intervention would have to take place,” said Aditya Saraswat, MENA research director at Rystad Energy.

Amid the backdrop of international pressure, Iran’s economy has faced enormous constraints, with inflation standing at 40% as the government’s total budget only nominally increased from US$98bn to US$111bn in the past year. National Iranian Oil Company (NIOC) is officially entitled to 14.5% of total oil and gas exports, which stood at 1.85mn bpd in the current budget. However one-third of oil exports were handed over to the Islamic Revolutionary Guard Corps (IRGC), and expected oil exports have now dropped to 1mn bpd, while the benchmark oil price has been lowered to US$57 per barrel from US$63 per barrel, reducing NIOC’s total receivables.

In addition, many of Iran’s core producing assets are in late life and experiencing steep natural declines. Underinvestment in maintenance, workovers and pressure support will accelerate the decline rates of these legacy fields. Many gas fields have complex structures and low recovery rates that pose challenges for local contractors. With assets under pressure, Iran’s NDF, which was designed to preserve a share of oil and gas revenues for future generations, continues to be treated as a source of near-term financing.

“From the regime’s point of view, the only redeeming factor in this situation is China’s role as the key driver of export revenues. As it stands, China accounts for 90% of Iran’s oil exports, with even a portion of cargoes booked for ‘unknown’ destinations ending up in China. Although the current export model looks feasible in the near term, its sustainability is becoming more conditional,” Saraswat said.

The recovery of Iran’s exports has been driven mainly by discounting, with additional costs incurred by measures required to evade sanctions, such as operating a shadow fleet. Without access to conventional banking channels, Iran relies on yuan-denominated accounts, barter arrangements or circuitous money-laundering pathways that extract substantial commissions. These structural inefficiencies mean Iran receives only two-thirds of benchmark oil, threatening Iran's ability to make a profit, even amid low upstream breakevens of US$20 to US$25 per barrel.

“Iran’s survival under sanctions reflects a mix of sustained upstream investment, strong trade relationships and covert workarounds. The continued brownfield redevelopment of mature fields has helped keep output stable, while contracts awarded to local players have added incremental volumes. However, a heavier reliance on China has drawbacks for Iran. Its margins will weaken as shadow logistics and intermediaries are priced in, and demand could be volatile as quotas and refinery runs change,” Saraswat concluded.

Pressure grows on Iran's oil sector and economy