The conflict in the Middle East could result in repair and restoration costs for energy infrastructure of up to US$58bn, with the speed of recovery depending on how quickly operators can secure access to constrained supply chains, says Rystad Energy

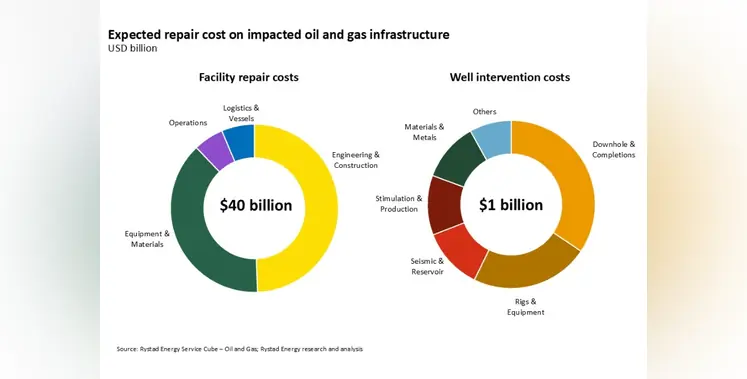

Overall, repair costs for the oil and gas sector are estimated at between US$30-50bn, with non-hydrocarbon infrastructure including aluminium smelters, steel plants, power stations and desalination facilities adding a further US$3-8 bn.

The main constraint to recovery, is access to equipment, contractors and logistics, with repair activity and the restoration of existing production being prioritised over new project execution and greenfield developments.

Rystad notes the divergence in recovery paths between countries and assets, with some facilities where damage was contained and contractor capacity was already present being able to resume operations within weeks, particularly where work is limited to surface equipment and modular repairs. In contrast, recovery could take years where facilities require construction of core process units or are dependent on long-lead equipment .

Downstream refining and petrochemical assets account for the largest share of repair costs, reflecting their complexity and the extent to which they were impacted in the later stages of the ongoing war. Midstream and upstream assets follow, while wells and industrial infrastructure are less impacted.

Iran accounts for the highest number of impacted facilities with repair costs potentially up to US$19bn, with damage sustained across the value chain, with simultaneous disruption to processing, refining storage and exports. Restoration and repair will likely take longer than elsewhere in the Gulf due not only to the damage incurred but also because of lack of access to western EPC contractors, OEMs and technologies.

In Qatar, damage is centred on Ras Laffan Industrial City, where multiple LNG trains have been affected alongside disruption at the Pearl gas-to-liquids facility. Redirection of capacity towards repair activity could lead to delays in ongoing expansion projects such as the North Field expansion.

Recovery timelines are less dependent on on-site execution and the scale of impact and more on how quickly operators can secure access to constrained supply chains says Rystad.

“What is emerging is less a reconstruction programme and more a competition for access – access to equipment, contractors and logistics capacity.

“Those that move early will secure capacity and shorten timelines, while others may face delays that extend well beyond the physical scope of damage.”

Karan Satwani, senior analyst, supply chain research commented, “This is no longer just a story about damaged facilities in the Gulf. It is a stress test for the global energy supply chain.

“The same equipment and contractors needed to rebuild are already committed to a wave of LNG and offshore projects sanctioned since 2023.

“Repair work does not create new capacity, it redirects existing capacity, and that redirection will be felt in project delays and into inflation far beyond the Middle East.

“The US$58 bn bill is the headline, but ththe knock-on effects on energy investment timelines globally may prove just as significant.”

Energy infrastructure repair bill could reach US$58bn: Rystad