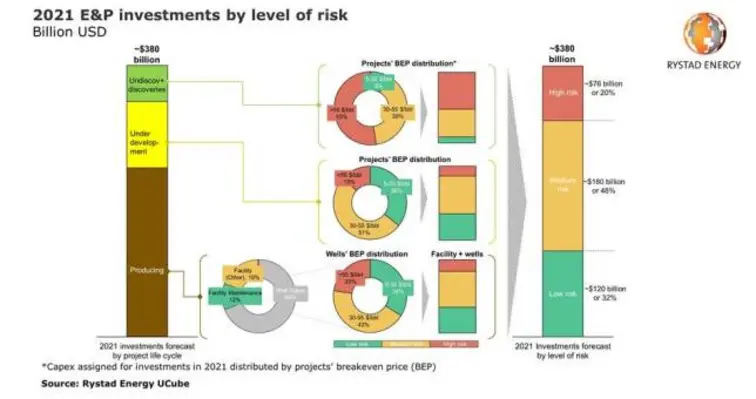

Investments from global exploration and production companies (E&P) in 2021 are projected to reach around US$380bn, almost flat y-o-y, according to Rystad Energy report

About 20% or US$76bn of the estimated 2021 investments could be at risk of deferral or reduction, with the remaining amount being categorized in the safer tiers of low and medium-range risk.

The amount is our base case scenario, but with 2020’s market turbulence fresh in mind and the currently uncertain roll-out timing of the recently announced COVID-19 vaccines, it’s worth expanding the forecast to a range of US$350bn to US$430bn, incorporating some scenario deviation.

Investments may rebound to the pre-crisis level of US$530bn by 2023 if oil prices rise to around US$65 per barrel – though we should keep in mind that after the previous market crisis in 2014, annual E&P investments never recovered to the pre-crisis level of about US$880bn and instead settled at US$500bn to US$550bn.

Much of that reduction was due to supply chain and efficiency improvements, leaving little scope for further such reductions this time around. Instead, E&P players are pulling other levers to weather this market downturn, such as deferring infill drilling programmes, projects FIDs and start-ups, reporting significant write-offs on stranded assets, and reshaping their portfolios to stabilise returns.

“As E&Ps are also speeding up a transition into low-carbon energy, it is possible that this time, too, upstream investments will not return to pre-crisis levels in the long-term, even if they do recover somewhat over the next few years,“ said Olga Savenkova, upstream analyst at Rystad Energy.

Of the total US$380bn of projected investments, about 60% (US$234bn) is likely to come from producing assets, which have two main spending channels: facility and well capex. Within facility capex, about 38% is spent on facility maintenance. This is believed to be a low-risk category, as operators were forced to postpone most of their planned maintenance programmes in 2020 due to coronavirus restrictions and lower oil prices. Maintenance work will therefore have high priority in 2021 to avoid unplanned outages in the future.

Well capex is split by the wells’ breakeven price, which gives a clear idea of how much of it might be at risk of deferral or repeal due to lower oil prices. About 23% (US$37bn) of the total well capex is assigned to wells with a breakeven price higher than US$55 per barrel, which puts this spending at high risk of deferral. Wells with breakeven price in the range of US$30 to US$55 per barrel are seen as medium risk, while those with a breakeven below US$30 per barrel are low-risk drilling opportunities.